An Income Earthquake- Sequencing Risk

- Mar 3, 2017

- 5 min read

Income earthquakes wreak permanent devastation to anyone drawing an income from their investments. Like an earthquake, sequencing risk occurs without warning. It shakes the solid ground you thought you were standing on and it cannot be prevented. Its also totally random, and they will always occur. You can however shore up the structure of your investment to withstand its impact.

Its the biggest risk income investors (such as retirees) face when investing is in the first five or so years.Sequencing Risk is defined as when you experience relatively poor returns (and a few potholes) in the early years for a retirement that perhaps has to span 25-30 years.

Like an earthquake it can ruin a happy secure retirement even if starting with the right amount saved. 2008 (the GFC) and 2011 (The great Recession in the USA) were recent examples. For those unlucky enough to have retired on or just before either, the amount you could then live on had to be cut drastically, or face the likelihood of the money running out and living their last years in poverty or being forced to sell one’s home. This doesn’t have to happen. In this article we will look at historic examples and what can be done to mitigate this risk.

It can happen no matter what you invest in including property, unless you take the right precautions. For most people holding shares of productive businesses is a part of the long term need to earn enough growing income to ensure a secure 25-30 retirement - A second lifetime of living. Shares are also the most volatile, and so we will use this asset class in our examples.

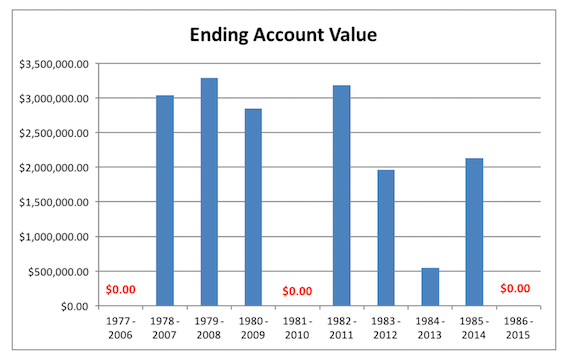

A Case study - 10 Couples retiring: Each couple saved a nest egg of $1 million, investing into the top 500 USA companies– The S&P 500 Index (a similar outcome applies investing in the Top 200 Australian businesses- ASX 200).

Rising life expectancy means 25-30 years income is required. Each withdraws $100,000 p.a. increasing by 3% p.a (countering inflation). Fees and taxes are removed as they don’t alter the comparative outcome. Each couple retires one year after the other starting in 1977 (the last couple retiring in 1987).

How did each couple fare?

3 ran out of money well before 30 years simply because they retired one year too early or too late in hindsight.

7 ended well with balances from $500,000 to $3.2 million.

Its random. Who ends up where however is totally random - skill has little impact.

How not to be one of the three. The three that ran out of money retired in 1977, 1981, and 1986. Their ‘average’ returns were still respectable, and compared to those whom did not run out, sometimes achieved even better. So how could they have found themselves in this awful mess? The first five to 10 years of their investment, returns were subpar. Even though later they did well – better than others whose middle to back end of retirement experienced more mediocre returns.

Insight 1: The perfect storm for retirees is when unexpected catastrophe type losses occur combined with sub-par returns in the early years. You get so far behind; it becomes impossible to catch up. It’s known as “sequence of returns risk.”

It’s like an ever decreasing spiral that at each income payment point, more capital is required, which deprives one of that capital in the future to build more income- forever!

The results for each couple

Random and bad- with a twist! When analysing the declines for in the S&P there were 15 random periods of negative moments of -10.2% to -56.8% lasting from 33 to 929 days. Yet overall returns were very healthy as we can see in the next table. There is no way to predict who would have been the unlucky 3 and who weren’t. There is no pattern or warning bell. An adviser cannot confidently avoid this from happening; but there are precautions one can take.

...The twist. Although over the long term the S&P returned 1.48% more per year for 1977 to 2006 (the worst couple enjoyed this higher average overall return) than the couple from 1979 to 2008 (the best resulting account couple of all 10), the former couple, who's longer term average return was greater....... ran out of funds.

It was the first five or so years of relatively higher investment returns (and no big losses) that the best couple enjoyed, than the worst couple who retired in 1977.

Insight 2: Be wary of chasing the highest returning investments appearing on league tables. These results are too hard to sustain. What matters is that in the first period of retirement you don’t fall below a reasonable return (not out performing it), and also not falling into catastrophic potholes. On average potholes lasting more than 3 months occur once every 6 years.

No one can predict when either. Since 1930 they struck 20 times; 9 lasting over 300 days - the longest 929 days (Year 2000). Even though the rises over time will provide an average return outperforming other forms of investment, it is the retiree’s need of constant draw-downs without periods of sub-par results in the early years, which interferes with a happy and secure future.

Insight 3: Holding most of your savings in real property won’t shield you from this risk. At some point the rental income alone will not suffice and even though a large amount is not needed in any month you can’t sell just a few bricks; and so the inevitable property sale will take place. At this point the whole sequential risk event begins for this portion of a nest egg all over again. Placing it all in cash creates an equivalent disaster.

Having your cake and eating it too! The reality facing retires is the need for exposure to large amounts of liquidable growth assets even though their volatility can be damaging. Here is how to enjoy its benefits and reduce sequential risk.

Keep 2 years income in a cash type account so you can ride out most periods of low/negative returns

Invest in equity funds that aim to produce a growing portion of income

‘Dollar cost average’ your nest egg into the retirement strategic asset allocation (if not already set up in this way)

Diversify in ways that smooth out returns without giving up to much upside.

‘Downside protect’ a good portion of your equity investment. Managed funds that deploy capital protection in equities are a good start.

Finally, when retired, having the highest performers is not as important as smoothing out the inevitable ‘potholes’ across your portfolio. Don’t try, as it increases risks you don’t need. Shielding a nest egg is as crucial as posting good above inflation returns. Stellar performers often experience stellar losses. Beware.

Happy investing, Grant.

Comments